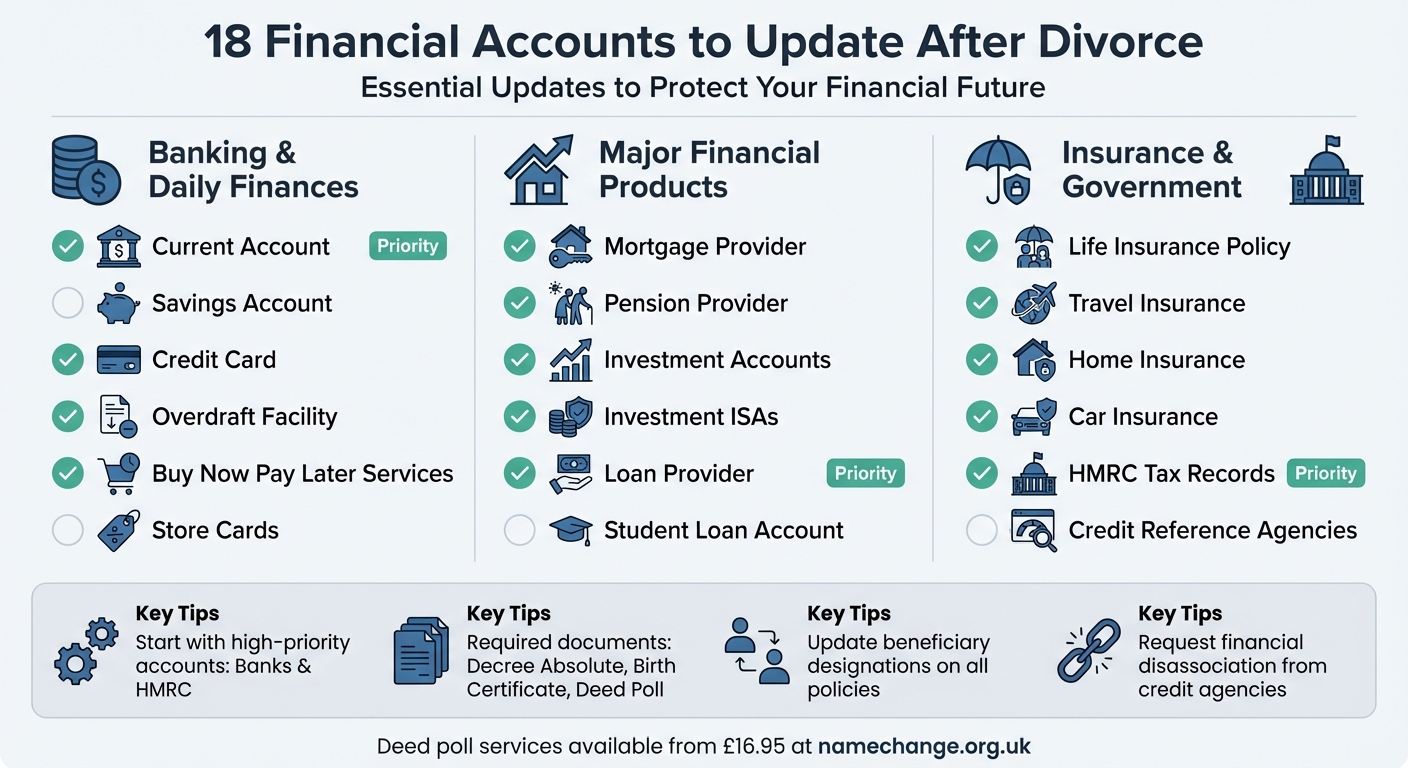

18 Financial Accounts to Update After Divorce

Divorce is a major life change, and updating your financial accounts is essential to avoid complications like identity verification issues or delays in transactions. Here’s a list of 18 accounts you should prioritise updating:

- Current Account: Visit your bank with legal proof (e.g., Decree Absolute or deed poll) to update your name.

- Savings Account: Similar to your current account but may require additional steps for joint or online accounts.

- Credit Card: Submit legal documents to your provider to ensure your name matches your credit records.

- Mortgage Provider: Align your name with HM Land Registry records to avoid refinancing issues.

- Pension Provider: Update your name and beneficiary designations to secure future benefits.

- Investment Accounts: Ensure your records match HMRC files to prevent tax complications.

- Life Insurance Policy: Change your name and beneficiaries to reflect your current situation.

- Travel Insurance: Match your policy name with your updated passport to avoid travel disruptions.

- Home Insurance: Update your name and remove your ex-spouse if applicable.

- Car Insurance: Inform your insurer to keep your policy valid and accurate.

- HMRC Tax Records: Update your name to avoid tax errors or mismatches.

- Student Loan Account: Notify your provider to prevent penalties or repayment issues.

- Buy Now Pay Later Services: Ensure your name matches your bank account to avoid missed payments.

- Investment ISAs: Update your name and review beneficiary details.

- Overdraft Facility: Confirm your overdraft reflects your updated current account details.

- Store Cards: Contact providers with legal proof to update your name.

- Loan Provider: Inform your lender to keep your credit history aligned.

- Credit Reference Agencies: Ensure your updated name is reflected and request a financial disassociation from your ex-spouse.

Key Tip: Use a deed poll to simplify the name change process across institutions. Services like Name Change (starting at £16.95) can help with legally valid documentation.

Updating these accounts ensures your financial records are accurate, prevents delays, and safeguards your identity. Start with high-priority accounts like banks and HMRC, then move on to others. Understanding how long a name change takes can help you manage your timeline effectively.

18 Financial Accounts to Update After Divorce Checklist

1. Current Account

Your current account is the central hub for most of your day-to-day financial activities, making it one of the first accounts you should update after a divorce. Before heading to your bank, ensure you understand how to change your name and the process is finalised. If it isn’t, you can use a legally valid deed poll through Name Change (https://namechange.org.uk).

In the UK, banks typically require an in-branch visit to update your name. This policy helps safeguard against identity theft and fraud. When visiting, you’ll need to bring your original Decree Absolute (or a professionally translated version if the document isn’t in English and your divorce occurred abroad). If you only have a photocopy, it must be officially certified by a professional, such as a solicitor.

If you’re reverting to your maiden name, you’ll need additional proof that links your former and new names, such as your Decree Absolute and birth certificate. The processing time for name changes varies by bank, with most completing the update within a few business days to two weeks. For example, Tesco Bank handles requests by post and typically processes them within 10 business days after receiving your written request and supporting documents. Importantly, your account details, like your sort code and account number, won’t change during this process.

If visiting a branch isn’t feasible, some banks, including Barclays and Tesco Bank, allow you to update your name by post, provided you send certified copies or original documents. Additionally, if you bank with Lloyds Banking Group, updating your name with them will automatically update your details across their other brands, such as Halifax, Bank of Scotland, and MBNA. Once the change is complete, don’t forget to request a new debit card and chequebook with your updated name.

After updating your current account, move on to your savings account to ensure all your financial records are consistent.

sbb-itb-bf1bef6

2. Savings Account

Updating your savings account follows a similar process to changing your current account details and understanding the legal implications of changing your name, but there are a few extra steps to consider, especially for online providers and joint accounts.

For major UK banks like HSBC, Barclays, NatWest, and Lloyds, you’ll need to visit a branch with your Decree Absolute and valid ID. If you’re reverting to your maiden name, you’ll also need to bring your birth certificate to connect your previous and current names. Tesco Bank, on the other hand, handles updates by post. They process requests within 10 business days after receiving your original documents.

For online-only providers such as Close Savings, you’ll need to provide a recent bank statement (dated within the last three months) from your current account that reflects your new name. Once your completed form and supporting documents are received, they typically process the update within five working days.

If you share a joint savings account with your ex-spouse, both account holders usually need to sign the request or provide identification to proceed with the name change. The account number and sort code remain the same, ensuring standing orders and direct deposits continue without disruption.

When handling multiple accounts via post, it’s a good idea to have a professional certify copies of your Decree Absolute instead of sending the original. This way, you can safeguard your key legal documents while updating several accounts at once.

3. Credit Card

To update your credit card after a name change, you'll need to provide legal proof of the change. This is important for fraud prevention and regulatory compliance. Make sure your name change is legally final before proceeding. If you need a secure and legally valid deed poll, you can use resources like Name Change.

"You'll need to show us clear copies confirming your new name... This helps us protect you from fraud, and it's one of our regulatory responsibilities."

The documents required depend on your situation. If you're reverting to your maiden name, you'll need your Decree Absolute and original marriage certificate. For a completely new name, submit a witnessed deed poll or statutory declaration.

The process for updating your credit card varies depending on the provider:

- Barclaycard (Standard Accounts): Send clear copies (not originals) of your documents by post to the Customer Relations Department at PO Box 9131, 51 Saffron Road, Leicester, LE18 9DE.

- Amazon Barclaycard: Bring your original documents and card to your local Barclays branch.

- HSBC: Typically requires an in-branch visit with your Decree Absolute and proof of your previous name, such as a passport or driving licence.

Once your name has been updated, request a new physical credit card to reflect your legal identity. If you share a joint credit card with your ex-spouse, remember that both parties are still responsible for the debt until the account is formally closed or restructured. As Bari Zell Weinberger, Managing Partner of Weinberger Divorce & Family Law Group, explains:

"This prevents a hurt spouse from running up 'revenge debt,' and it also makes it easier to divide the debt in the divorce because it creates a clean break."

If your divorce documents aren't in English, ensure you get a professional translation. Most credit card providers don't charge for name updates. After completing this step, consider updating your mortgage provider to keep your accounts consistent.

4. Mortgage Provider

Changing the name on your mortgage isn’t just a simple administrative update - it involves legal documentation that must align with HM Land Registry records. Most lenders offer two options for updating your name: you can visit a local branch in person or send your original or certified documents to their mortgage administration department by post.

For those reverting to a maiden name, you’ll usually need a certified copy of your Decree Absolute and your original marriage certificate. If you’re adopting a completely new name, you’ll need to provide a witnessed deed poll. Make sure your deed poll meets all legal requirements. Alongside these documents, lenders will also ask for at least one form of personal ID, such as a passport or driving licence.

Don’t forget to update your name on the property title deeds with HM Land Registry. If the name on your mortgage account doesn’t match the Land Registry records, lenders may decline future refinancing or mortgage applications. HM Land Registry emphasises:

It's common for lenders to refuse to lend money unless your details exactly match the register.

To update the Land Registry, use Form AP1 - there’s no charge for this service.

If you’re removing an ex-partner’s name from the mortgage, this involves a "Transfer of Title" rather than a straightforward name change. This process requires a full affordability assessment and legal assistance from a solicitor. Malcolm Davidson, Managing Director of UK Moneyman Ltd., highlights:

Until a name is officially removed from the mortgage, the lender will see both parties as liable.

It’s best to wait until court proceedings are finalised before starting this process to avoid complications or expired applications. This ensures that all property records remain consistent with your updated financial details with your updated financial details.

Once your mortgage is updated, take the time to review your buildings and contents insurance policies. Ensuring they reflect your new details is essential to keep them valid.

5. Pension Provider

After updating your current accounts and mortgage, it's important to also update your pension provider details. This helps keep your financial records consistent and ensures your benefits are safeguarded.

Most pension providers allow updates through online portals, over the phone, or by post. If you have a workplace pension, your employer will handle updates through their regular data submissions. If you're already receiving pension payments, you'll need to contact your provider directly. For State Pensions, you can call 0800 731 0469 or manage your details online.

To update your records, you'll need to provide proof of a name change. This is typically done with a copy of your Decree Absolute or a deed poll certificate. If you haven't legally changed your name yet, a deed poll can serve as the required documentation. According to TPT Retirement Solutions:

If you have changed your name, we need to see the original documentation or a certified certificate to validate the change before any payments can be made.

Additionally, you'll need to review and update your beneficiary designations. Divorce often invalidates any previous death benefit nominations unless the nominee is someone you later married. TPT Retirement Solutions explains:

Upon marriage and divorce, any previous nominations for death benefits that you may have made are void (unless you married your recorded nominee).

To ensure your wishes are clear, complete a new "Expression of Wish" or "Nomination of Beneficiaries" form as soon as possible. This ensures any lump-sum death benefits go to the intended recipient. Keeping your pension records up to date is a crucial step in protecting your future benefits.

6. Investments Account

Updating your investment accounts to reflect your new name is crucial to avoid potential tax or regulatory complications. Before starting, ensure your legal name change is fully processed. Services like Name Change can help simplify the steps involved.

If you manage investments through platforms like Vanguard, Hargreaves Lansdown, or Fidelity, make sure to update your name on these accounts. It’s essential that your investment records align with HMRC files to prevent tax reporting issues. Fidelity highlights the importance of this:

Make sure your name matches what's on file with the IRS. If there's a discrepancy, the IRS might require Fidelity to withhold taxes from your transactions.

In the UK, most investment providers will request your Decree Absolute as the main document for name changes. However, if you’re reverting to your maiden name, additional proof may be required. For instance, Hargreaves Lansdown will ask for your Decree Absolute along with one of the following: a marriage certificate, birth certificate, or deed poll to link the name change. Similarly, providers like Close Savings may require a recent bank statement (dated within the last three months) showing your updated name on your nominated account.

Documents can typically be submitted via online upload, mobile verification, or by post with certified copies. For example, Hargreaves Lansdown processes name changes within 2–3 working days, while Close Savings aims for completion within five working days.

It’s also a good time to review your beneficiary designations. Divorce does not automatically remove an ex-spouse from all investment-related death benefits. To ensure your intended recipient receives any lump-sum benefits, you may need to complete a new "Expression of Wish" form. As Fidelity UK explains:

Although your ex-partner is automatically cut out of your will as soon as your divorce is finalised, the rest of your will remains valid.

For postal submissions, have your documents certified by a recognised professional. They should confirm that "the copy is a true and complete copy of the original" and include their contact details and professional designation.

Once your investment accounts are updated, move on to revising your life insurance policy to keep all financial records consistent.

7. Life Insurance Policy

After a divorce, it's crucial to update your life insurance policy to ensure your intended beneficiaries are protected. Remember, a divorce doesn’t automatically remove an ex-spouse’s entitlement unless their name is formally changed on the policy.

Most insurers make the name update process straightforward. You can usually do this online, over the phone, or by submitting a written request. Be prepared to provide original or certified copies of documents like your Final Order (previously known as the Decree Absolute), marriage certificate, and birth certificate. If you don’t have the originals, a deed poll can serve as evidence, and replacement certificates can be ordered from the General Register Office for about £11 each. Services such as Name Change can guide you through the deed poll process if needed.

For joint policies, things can get a bit more complex. You might need to remove a name, transfer the policy to one individual, or split it into two separate policies using a "separation benefit." It's important to act quickly on these changes. If your policy is held in an Absolute Trust, the named beneficiaries generally cannot be altered. However, with Discretionary Trusts, updates are usually possible.

Before making changes, double-check that your new beneficiary details align with any court-ordered settlements or financial plans. Contact your insurer for a beneficiary change form and ensure everything matches your legal agreements. Peter Johnson, a divorce lawyer at Alexander JLO, highlights the importance of this step:

A policy beneficiary nomination can override intestacy rules and direct proceeds to a named person.

If you’re thinking about switching to a new provider, don’t cancel your current policy until the new one is active. This avoids any gaps in coverage. Keep in mind that life insurance premiums are generally lower when you’re younger, so switching policies later might result in higher costs compared to your original plan.

8. Travel Insurance

After a divorce, it's essential to update your travel insurance right away, especially if you're returning to your maiden name. The name on your policy must match your passport exactly; otherwise, you might face denied claims, boarding delays, or even issues accessing medical care while abroad.

If your coverage was tied to your ex-spouse's multi-person or family policy, that protection will likely end once the divorce is finalised. Reach out to your insurer to arrange individual coverage. Lynn Toynton, an Insurance Adviser at Partners&, advises checking for duplicate coverage before making changes:

Are you paying for travel insurance via your bank and a stand-alone policy? If so, let's get rid of one.

Many premium bank accounts already include travel insurance, so confirm what you have before purchasing a new standalone policy.

When updating your policy, you'll need to contact your insurer’s customer service team with your Final Order (previously called a Decree Absolute) ready. Before that, update your passport (£94.50 online, £107.00 by paper application) so that your documents align.

Timing is crucial. If you've already booked travel under your married name, you’ll need to either pay to update your reservation or travel using your old documents (if they’re still valid) to avoid any mismatches. Matthew Wolff from HitchSwitch emphasises the importance of this:

Consistency is key. Any discrepancy between identification documents and travel books may result in delays, denied boarding, or other travel disruptions.

Make sure all travel documents match your updated name to keep everything consistent with your financial records.

If your legal name hasn’t changed, you can use Name Change (https://namechange.org.uk) to quickly update key documents, including your travel insurance.

Lastly, update your emergency contact details to remove your ex-spouse and ensure any death-in-service benefits no longer list them. Aligning your travel insurance details with your updated financial accounts will help you avoid future complications.

9. Home Insurance

After a divorce, it's essential to update your home insurance to reflect your new legal identity. This could mean changing your name or removing your ex-spouse from the policy. The name on your insurance must match the official property records to avoid potential issues with claims or remortgaging. As HM Land Registry points out:

One of the biggest cause of delays when dealing with property is when a name is different from the name recorded in the register.

Most insurers allow you to update your details online, through live chat, or over the phone. Be aware, though, that fees can vary depending on the method. For instance, Ageas charges £20 for updates made outside of their online system, while online updates are free.

To confirm a name change, you'll need to provide a certified copy of your Final Order and marriage certificate. If you're removing an ex-spouse from a joint policy, insurers typically require written agreement from both parties.

Don't forget to update HM Land Registry records as well, using Form AP1. Chris Sweetman, Solicitor and Founder Director of Fair Result, highlights the importance of this step:

Financial institutions such as mortgage and pension companies... will only amend their records after viewing the official paperwork.

While you're making these updates, it's a good idea to review your buildings and contents insurance to ensure it reflects any changes in circumstances following your divorce.

10. Car Insurance

Updating your car insurance after a divorce is crucial to avoid invalidating your policy or facing issues with claims. Like other financial accounts, ensuring your car insurance reflects your legal name is essential. As Aviva highlights:

It is important to tell your car insurer about any changes, as incorrect information on your policy could impact any settlement if you need to claim.

Most insurers allow you to update your details either online or over the phone. Make sure you have your policy number and new name details ready. Keep in mind that some insurers may charge an administration fee for mid-term changes, though online updates often come with reduced fees. Louise Thomas, a motor insurance expert, notes:

Many insurance companies let you change your details online, and you might be able to get a reduced admin fee for doing so.

It's important to remember that updating the DVLA does not automatically update your insurer's records. Even after updating your driving licence and vehicle log book (V5C), you must contact your insurer directly. This step ensures your car insurance details remain accurate.

If you're removing an ex-spouse as a named driver or changing your address, inform your insurer right away. A change in marital status from "married" to "divorced" could lead to higher premiums, as you may lose certain discounts. Additionally, staying listed as a "named insured" on a joint policy could leave you financially and legally liable if your ex-spouse is involved in an accident.

For a legally recognised name change, consider using Name Change (https://namechange.org.uk) to ensure your new name is updated across all relevant institutions.

11. HMRC Tax Records

After updating your insurance and mortgage accounts, make sure to refresh your HMRC tax records as well. This step is crucial to avoid potential tax errors or unexpected bills. As highlighted on GOV.UK:

Tell HMRC straight away – if you do not, you could pay too much tax, or get a tax bill at the end of the year.

You can update your details conveniently online through your HMRC Personal Tax Account or the HMRC app. If you're paid via PAYE (whether through salary or pension), updating your information online typically updates both your Income Tax and Self Assessment records automatically. Many people find that the HMRC digital assistant provides sufficient guidance for this process.

A key point to remember: HMRC does not inform your employer of a name change. You’ll need to notify your employer’s payroll or HR department directly to ensure that PAYE submissions align with HMRC records. This helps prevent Real Time Information (RTI) mismatches. Additionally, if you receive Child Benefit, you must separately report name changes for yourself or your child, as this is not linked to your main tax records.

If you're reverting to your maiden name, HMRC will typically require your marriage certificate and decree absolute (or final order) as proof. On the other hand, if you're adopting a completely new name, a deed poll will be necessary to provide legal evidence of the change.

When contacting HMRC, make sure to have your National Insurance number handy. If you need to call, it's best to do so before 10:00 am, as the lines are usually less busy during this time. Importantly, there’s no charge for updating your name or personal details with HMRC.

Once you've updated your HMRC records, it’s a good idea to review your student loan account details next.

12. Student Loan Account

If you've changed your name, it's crucial to update your details with Student Finance England (or Student Finance NI if you're in Northern Ireland). Not doing so could result in financial penalties or higher interest rates for non-compliance.

To make the update, you'll need to send a signed and dated covering letter. This letter must include your Customer Reference Number (CRN), details of the change, and the reason for it. Without this information, the Student Loans Company won't process your request:

"The covering letter must be signed and dated by you, confirming what change is to be made and the reason for the change, otherwise we'll not be able to make the requested change".

Additionally, you'll need to provide a photocopy of your decree absolute, final order, or conditional order as proof of your name change. For faster processing, upload the evidence online. Alternatively, you can post it to Student Finance England, PO Box 210, Darlington, DL1 9HJ. Keep in mind that postal submissions can take up to four weeks to process.

If you've completed your course and are already repaying your loan, you should call 0300 100 0611 to report the name change. Should your bank account details also need updating, make sure to notify them at least four working days before your next scheduled payment.

It's worth noting that a name change won't impact your repayment plan or loan terms. These are based on when and where you studied, not your marital status. However, updating your marital status is still important if you're currently studying, as it could affect your household income assessment. This, in turn, might increase your Maintenance Loan entitlement.

Once you've updated your student loan account, don't forget to move on to updating any Buy Now Pay Later services.

13. Buy Now Pay Later Services

Make sure your legal name is updated across all official records. For affordable deed poll services, you can consider Name Change (https://namechange.org.uk).

Services like Klarna and Clearpay, which fall under the "Buy Now Pay Later" (BNPL) category, are classified as credit providers. This means they must reflect your current legal name. If your personal details don't match official records, it could lead to delays or even rejections when applying for credit in the future. These accounts are often overlooked during post-divorce updates because they’re tied to shopping apps, but they form an important part of your overall financial profile. Ensuring consistency across all financial accounts after a divorce is crucial.

Most BNPL providers offer straightforward ways to update your name via their mobile apps or websites. Look for options like 'Manage Personal Details' or 'Settings'. If these aren't available, you can email their customer service team with certified documents, including your account number. Typically, you'll need to provide your Final Order (formerly Decree Absolute) and proof of identity with your new name, such as an updated passport or driving licence. If you're returning to a maiden name and your marriage certificate links both names, some providers may accept this as sufficient evidence.

Before reaching out to your BNPL provider, update the name on your linked bank account or debit card. These services often rely on Continuous Payment Authorities, which can fail if the name on your card doesn’t match the account holder’s name. This could result in missed payments being reported to credit reference agencies - a record that can stay on your credit file for six years. By aligning your BNPL accounts with your updated bank details, you can avoid these potential issues.

Additionally, update any BNPL account passwords that may have been shared with your ex-spouse. Comerica highlights the importance of this step:

Making a clean separation of your finances early can help reduce complications later on when it is time to formally divide assets. It is also a good way to keep your credit score healthy, as a spiteful ex-partner can potentially damage your credit score with overzealous spending.

These measures not only safeguard your credit record but also help you achieve a clean financial break. After completing these updates, you can move on to reviewing your Investment ISAs.

14. Investment ISAs

Investment ISAs are personal accounts, and it’s essential that they reflect your current legal name to prevent any issues with withdrawals, transfers, or refinancing.

Most UK investment platforms will ask for your Decree Absolute as the main proof of your name change. Some providers, like Hargreaves Lansdown, might also require additional documents, such as your birth certificate, marriage certificate, or deed poll, to confirm the connection between your old and new names. For example, Vanguard accepts the Decree Absolute but has a specific process where you must upload the document to your online account and send a secure message to request the update:

If you need to change the name on your account, you must upload a document as proof of the change to your online account. When you have done that, you need to send us a secure message asking us to update your name.

Additionally, make sure your nominated bank account reflects your new name. To do this, provide a recent bank statement (dated within the last three months) before any changes can be processed. If you’re sending documents by post, ensure they are certified by a recognised professional. These steps help ensure that your ISA details are consistent with your other financial records.

If your legal name hasn’t been updated yet, consider using Name Change (https://namechange.org.uk), which offers a secure deed poll service.

While you’re updating your name, it’s a good idea to review your beneficiary details or "Expression of Wish" form. Your ex-spouse might still be listed, and this is a good opportunity to make adjustments. Next, move on to reviewing your Overdraft Facility.

15. Overdraft Facility

Your overdraft facility is tied directly to your current account, so when you update your current account, your overdraft typically updates automatically. However, it’s always a good idea to double-check that all records reflect your new name accurately. Before starting the process, confirm the specific requirements with your bank.

Most major UK banks - such as Barclays, HSBC, NatWest, and Lloyds - require you to visit a branch in person to change your name. Make sure to bring your Decree Absolute as legal proof. If you’re returning to your maiden name, you may also need to provide your birth certificate or marriage certificate to show the link between your previous and updated names. This helps ensure all your financial records stay consistent after your divorce. You can find more name change articles to help you navigate this process.

Some banks, like Barclays and Tesco Bank, offer the option to update your name by post if you send certified copies of your documents. For instance, Tesco Bank asks for a written request that includes your account number, old and new signatures, and the original Decree Absolute. To avoid losing important legal paperwork, make sure your documents are certified by a solicitor or bank official before posting them.

Once the change is processed, your bank will issue a new debit card with your updated name. Your account number and sort code will remain the same, so standing orders and direct debits will continue without interruption. Don’t forget to update any digital wallets, like Apple Pay or Google Pay, to ensure your physical and digital banking details match.

After the bank processes your name change, they will notify credit reference agencies to keep your credit history aligned with your new name. A few weeks later, check your credit file to confirm the update has been made. Once verified, you can move on to updating your store cards.

16. Store Cards

If you’ve recently gone through a divorce, updating your store cards is another important step to avoid future issues. Whether it’s an Amazon Barclaycard, a Tesco Bank card, or a New Look store card, each provider has its own process for handling name changes.

Generally, you’ll need to provide specific legal documents, such as a change of last name deed poll, as outlined by your card provider. For those returning to a maiden name, some providers might also ask for additional proof, such as a birth certificate or an updated passport to establish the link between your previous and current names.

Here’s a quick look at how some providers handle the process:

- Amazon Barclaycard: You’ll need to visit a Barclays branch or Barclays Local in person. Bring your card and the original name change documents with you.

- Tesco Bank: Send a written request to PO Box 343, Newcastle Upon Tyne, NE12 2GE. Include your account number, confirmation of the name change, and both your old and new signatures. They also require the original Decree Absolute, and if you’re reverting to your maiden name, a birth certificate or updated passport.

- New Look: Updates can be done by post or phone. For postal updates, send a letter with your old and new signatures, along with your Decree Absolute, to New Look Customer Services, Mercery Road, Weymouth, Dorset, DT3 5HJ.

Before sending any documents, it’s a good idea to call the customer service number on your card to confirm the specific requirements. If you’re mailing original legal documents like your Decree Absolute, use recorded or special delivery so you can track them and ensure their safe return.

If you encounter difficulties updating your details, consider opening a new account and transferring any loyalty points before closing the old one.

Once you’ve sorted out your store cards, don’t forget to update your loan provider information as well.

17. Loan Provider

Keeping your loan details up to date with your new name is a key step in ensuring consistency across all your financial accounts. Before reaching out to your lender, make sure your legal name change is finalised. If you're navigating a name change after divorce, Name Change (https://namechange.org.uk) offers a straightforward and secure service for those in the UK.

Whether it’s a personal loan, car finance, or another credit agreement, notifying your loan provider about your name change is essential. Having mismatched details can cause issues when applying for remortgages or new credit. As HM Land Registry advises:

It's common for lenders to refuse to lend money unless your details exactly match the register.

To update your name, contact your lender directly and provide the required documents. Most UK lenders will ask for a copy of your Decree Absolute and your original marriage certificate to connect your married name with your maiden name. You’ll also need updated identification, such as a UK passport or driving licence, in your new name. Each lender has its own preferred method for submitting these documents, so be sure to check their specific requirements.

Submission methods vary between lenders. For instance, Ikano Bank allows digital uploads of your Decree Absolute, while Lloyds requires certified originals sent by post. HSBC UK requests your Decree Absolute along with proof of your previous name, such as a driving licence or passport, and asks you to send originals via recorded delivery.

If you have a joint loan, both account holders remain equally responsible for the full payments until the account is legally updated or closed. To remove an ex-partner from a joint loan, the lender will typically perform an affordability assessment to ensure the remaining party can manage the payments alone. This process often involves a solicitor and may include administration fees.

Once your loan provider updates your name, they will report the change to credit reference agencies. To maintain consistency in your credit history, check your credit file after the update to ensure the changes are accurately reflected.

18. Credit Reference Agencies

When making updates to your financial accounts, it's equally important to ensure your credit reference information is accurate. This becomes especially critical after a divorce. Agencies like Experian, Equifax, and TransUnion maintain your credit history and verify your identity when you apply for financial products such as loans or mortgages. If your name isn't updated properly, you could run into problems when accessing credit.

The good news is that you typically don’t need to contact these agencies directly. When you update your details with banks, credit card providers, and lenders, they usually report these changes automatically. Credit reports are updated every 4–6 weeks. However, one key step you should take is updating your name on the Electoral Register by reaching out to your local authority. Don’t wait for the next election to make this change. Since credit reference agencies cross-check names and addresses with the Electoral Roll, this update is crucial for maintaining your credit score. It ensures all your financial records are consistent with your new identity.

Another important task is requesting a "notice of disassociation" from all three credit reference agencies. This formally breaks any financial ties with your ex-spouse. Equifax UK highlights the importance of this step:

Until the financial association is removed, financial actions from your associate could potentially impact your own credit report.

Make sure all joint accounts are either closed or converted before submitting this request.

After a few months, it’s a good idea to check your updated details by ordering a statutory credit report from each agency. These reports cost £2 and allow you to confirm that your name has been updated and any financial associations have been removed. If you spot any mistakes, you can file a notice of correction with evidence of your name change. Under GDPR regulations, the agency is required to address the issue within 28 days.

Here’s how to reach the main credit reference agencies:

| Credit Reference Agency | Contact Address |

|---|---|

| Experian | P.O. Box 8000, Nottingham, NG80 7WF |

| Equifax | P.O. Box 1140, Bradford, BD1 5US |

| TransUnion (formerly Callcredit) | P.O. Box 491, Leeds, LS3 1WZ |

Conclusion

Updating your financial accounts after a divorce isn't just a box to tick - it’s a critical step in protecting your financial well-being. Karen Axelton, Senior Personal Finance Writer at Experian, puts it plainly:

Changing your name on financial documents is a time-consuming process, but it's an essential step to safeguard your identity and finances and prevent future complications.

Leaving your accounts unchanged creates a host of potential issues. For instance, if the name on your credit application doesn’t match your credit report, you could face delays or even rejection, as changing your name can affect your credit score. HMRC may hold up tax refunds if your name doesn't match their records. And don’t overlook the DVLA - failing to update your name there could lead to fines.

The risks don’t stop there. Outdated beneficiary designations could result in your assets going to unintended recipients. If an ex-partner remains an authorised user on your credit cards, you might find yourself liable for debts they rack up. Even utility companies could disrupt your services if payments come from accounts under an incorrect name.

To make the process easier, Name Change offers a secure deed poll service for just £16.95. This includes printed documents, three certified copies, tracked delivery, and a detailed guide to help you notify all necessary institutions. Their service is recognised by all UK government departments and organisations, providing you with the official documents needed to update your financial accounts without hassle.

FAQs

Which accounts should I update first after divorce?

Start by updating essential government records, such as your passport, driving licence, and tax records. Once these are sorted, make sure to notify your bank and update your employer with your new personal details. Taking care of these updates promptly can help prevent issues with identification or financial transactions down the line.

What documents do I need to change my name everywhere?

To change your name after a divorce, you'll generally need a few key documents: your final divorce decree, original marriage certificate, and original birth certificate. If you're returning to your maiden name, you might also need to provide a signed statement and evidence of using your new name, such as a payslip.

If any of these original documents are missing, you can request replacements from the General Register Office. These documents are essential to ensure that any updates with organisations are legally acknowledged.

How do I remove my ex from my credit file?

To separate your ex from your credit file, start by closing and paying off any joint accounts you share. Once that's done, request a 'notice of disassociation' from credit reference agencies like Experian or Equifax. You'll need to provide evidence, such as divorce documents or proof of separate addresses.

If you're listed as an authorised user on their credit card, contact the card issuer directly to have your name removed. For joint loans or mortgages, you'll need to work with your lender to either refinance the agreement in one name or settle the outstanding debt entirely.