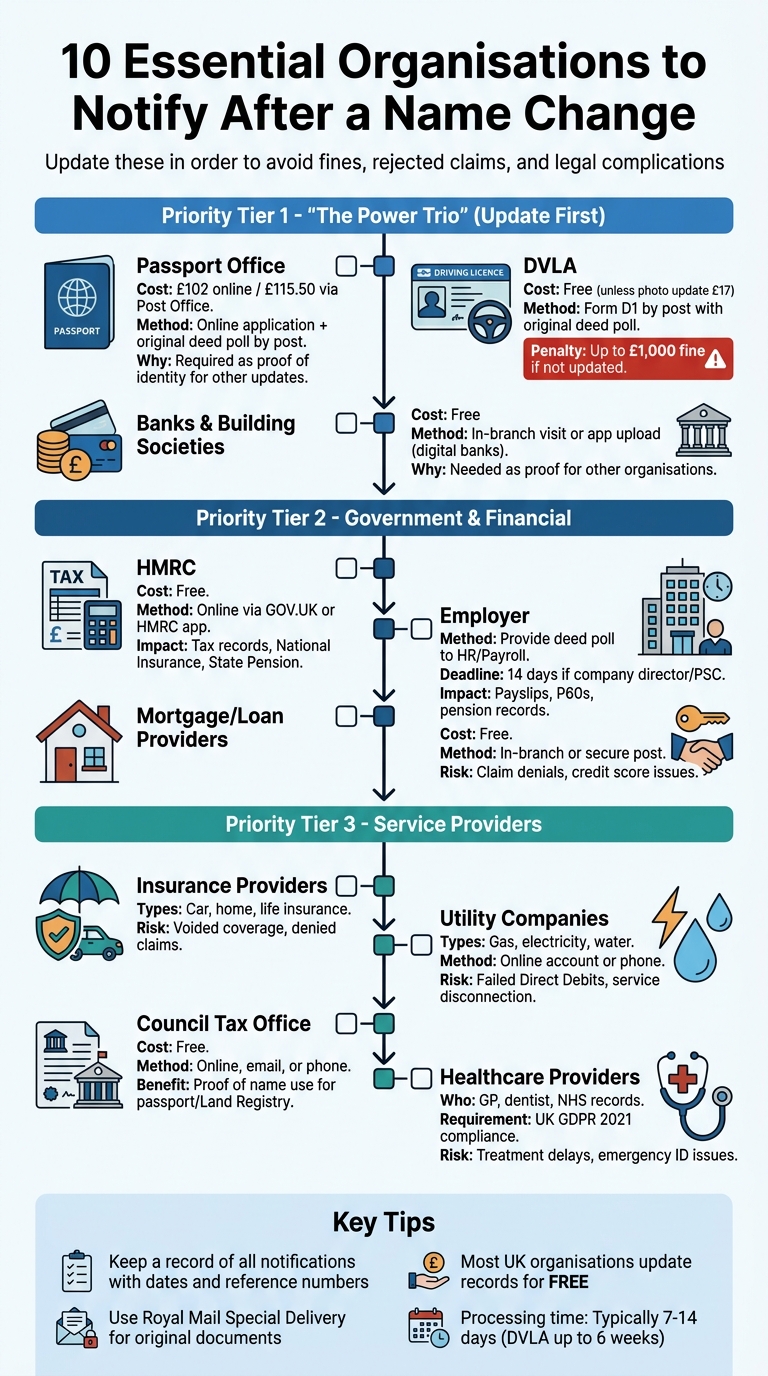

Top Organisations to Notify After a Name Change

Changing your name legally is just the first step. To avoid legal issues, financial disruptions, or mismatched records, you need to inform key organisations promptly. Here's a quick overview of the most important ones to notify:

- HMRC: Update your tax and National Insurance details to avoid mismatches.

- DVLA: Legally required to update your driving licence and vehicle logbook.

- Passport Office: Apply for a new passport to ensure your travel documents match your new name.

- Banks and Building Societies: Update your accounts, cards, and mortgage details to avoid payment issues.

- Employer: Ensure your payroll and pension records reflect your new name.

- Utility Companies: Keep your gas, electricity, and water accounts updated to prevent billing errors.

- Council Tax Office: Update your records for proof of name use and property-related matters.

- Insurance Providers: Align your policy details with your updated name to avoid claim denials.

- Healthcare Providers: Notify your GP, dentist, and NHS to ensure accurate medical records.

- Mortgage or Loan Providers: Avoid credit issues by updating your financial liabilities and records.

Why it matters: Failing to update your name can lead to fines, rejected claims, delayed payments, and even legal complications. Start with high-priority documents like your passport, driving licence, and bank account, as these often serve as proof for other updates.

Tip: Keep a record of all notifications and use certified copies of your deed poll when required. This ensures a smoother process and avoids sending out your only original document.

10 Essential Organisations to Notify After a UK Name Change

Why You Need to Notify Organisations

Changing your name via deed poll or other methods updates the legal document, but it doesn’t automatically update your details across all the organisations that hold your information. In the UK, your personal data is stored by a wide array of entities, from government agencies to financial institutions and service providers. If you don’t notify them, you risk errors and inconsistencies that could create administrative headaches.

Organisations can be grouped into three main categories:

- Government bodies: This includes HMRC, the DVLA, the Passport Office, and your local Electoral Registration Officer.

- Financial institutions: Banks, building societies, credit card providers, mortgage lenders, and pension schemes all fall under this category.

- Service providers: Utility companies, insurance providers, healthcare services, and employers are examples here.

Keeping your records consistent across these categories is essential for maintaining your legal and financial identity.

Failing to update your details can lead to avoidable problems. For example, direct debits might fail, resulting in service disruptions or late payment fees. Insurance policies can also become problematic - if your car insurance lists your old name but your driving licence shows your new one, any claims you make could be denied.

There are also longer-term consequences. If you don’t update your details on the Electoral Roll, your credit rating could take a hit. Similarly, fragmented records with credit agencies like Experian could temporarily split your credit history. And when it comes to HMRC, incorrect details could cause issues with your National Insurance contributions, potentially affecting your future State Pension.

The good news? Most organisations in the UK - such as banks, HMRC, and the DVLA - don’t charge for updating your records. To simplify the process, start with high-security documents like your passport and driving licence, as these are often required as proof of identity when updating other records. Next, we’ll look at how to notify these organisations efficiently.

sbb-itb-bf1bef6

1. HMRC (HM Revenue & Customs)

Legal requirement for notification

After changing your name by deed poll, it's essential to notify HMRC right away. Keeping your records consistent across government departments is a legal obligation. According to GOV.UK:

You need to tell HM Revenue and Customs (HMRC) if you've changed your name or address.

This helps prevent any future administrative headaches.

Impact on financial or legal documentation

Your new name must appear correctly on your tax and National Insurance records. If you run a business, you'll need to update your business records as well. For those filing Self Assessment returns, this update is especially important to ensure everything is accurate.

Ease of updating records

Updating your HMRC records is straightforward and free. The fastest way is through their online service or the HMRC app. Log in to your GOV.UK account and submit the change digitally. If you work with an accountant or tax agent, they can handle the process for you via their professional account, by phone, or through written communication. Keep your deed poll handy, as it may be required by other departments.

Potential consequences of failing to notify

If you don’t inform HMRC about your name change, it can lead to mismatches in your tax and National Insurance records. This could result in unnecessary delays and administrative issues for both individuals and business owners.

2. DVLA (Driver and Vehicle Licensing Agency)

Legal requirement for notification

Once you've updated HMRC, it's just as important to ensure your motoring records reflect your new identity.

By law, you must update your driving licence and V5C log book. According to GOV.UK, failing to notify the DVLA could result in a fine of up to £1,000.

Ease of updating records

The process is straightforward but needs to be done by post. Start by getting the correct form: D1 for cars and motorbikes or D2 for lorries and buses. These forms are available at your local Post Office. Fill out the form, and send it along with your old licence and the original document proving your name change. Keep in mind that photocopies or laminated certificates won’t be accepted.

For updating your V5C log book, complete the relevant section and include a short letter explaining the change. There’s no charge for this unless you’re also requesting a photo update (£17) or replacing lost documents (£20 for a licence, £25 for a log book). Be prepared for the process to take up to six weeks. If your vehicle tax is due to expire within the next four weeks, make sure to tax your vehicle online before sending off your log book.

Potential consequences of failing to notify

Not updating your DVLA records can lead to fines and create mismatches across your official documents. This could cause problems when renewing your insurance, taxing your vehicle, or handling other vehicle-related matters. Keeping your DVLA records up to date ensures that your driving licence and vehicle documents match your current identity, helping you avoid unnecessary complications.

3. Your Bank or Building Society

Impact on financial or legal documentation

Banks are responsible for maintaining essential financial records, such as account statements and mortgage documents. When you legally change your name, it's crucial that these records are updated to reflect your new identity. This ensures compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Failing to update your name can lead to delays in verification, rejected cheques, and issues with payments or transfers. Staying compliant helps avoid unnecessary financial and administrative headaches.

If you own a property, there's another step to keep in mind. While your bank will update the name on your mortgage account, this doesn't automatically update the Land Registry. Any mismatch between your bank records and Title Deeds can cause legal delays when selling or remortgaging your property. Updating the Land Registry is a separate process and should not be overlooked.

Ease of updating records

Traditional banks often make this process a bit more formal. For example, major banks like Lloyds, HSBC, and Barclays usually require you to visit a branch in person. You'll need to bring your original deed poll and photo ID. Request to speak with a Personal Banker who can assist with the update. While your account details - such as your account number, sort code, and Direct Debits - won't change, new debit and credit cards should arrive within seven working days.

On the other hand, digital banks like Monzo and Starling make the process much easier. You can typically upload a photo or a scanned copy of your deed poll directly through their app. Once the update is processed, the bank will notify credit reference agencies like Experian and Equifax, ensuring your credit history remains intact by linking your old and new names. Keeping your bank records up to date also aligns with the legal considerations discussed earlier.

Potential consequences of failing to notify

Failing to update your records can lead to breaches of GDPR and create delays in financial transactions. For instance, cheques signed with your previous name after a legal name change may be rejected. Similarly, discrepancies between your name and bank records can make it difficult to access credit under your new identity. If you're submitting documents by post, always use Royal Mail Special Delivery to avoid losing your original deed poll, as this can significantly delay the process. After the update is completed, make sure to dispose of old chequebooks to prevent confusion or errors.

4. Passport Office

Legal requirement for notification

Just like with HMRC, DVLA, and your bank, updating your passport is a crucial step when your name changes. If you plan to travel or need to confirm your identity, you’ll need to apply for a new 10-year passport. The HM Passport Office doesn’t amend existing passports, so a new application is required. Make sure the name on your passport matches the name used for booking travel, as discrepancies can lead to issues at the airport, including being denied boarding.

For those with dual citizenship, there’s an extra step to consider. You must first update your non-British passport to ensure both passports reflect the same name. This consistency is vital for smooth international travel and border checks.

Ease of updating records

Updating your passport is straightforward. You can apply online for £102 or use the Post Office Check and Send service for £115.50. You’ll need to provide your original deed poll as proof of the name change, which will be returned after verification. Unless your appearance has significantly changed since your last passport photo, a countersignature isn’t required.

Keep in mind that any remaining validity on your old passport won’t transfer to the new one. The new passport will be valid for 10 years from the date of issue and will have a different passport number. To avoid travel disruptions, don’t book any international trips until your updated passport arrives.

Potential consequences of failing to notify

If your old passport contains any unexpired visas, you’ll need to contact the relevant embassy immediately. A name change can render these visas invalid, potentially causing issues with planned travel. Not updating your passport can lead to legal and financial troubles, so it’s best to handle this promptly to avoid unnecessary complications.

5. Your Employer

Legal requirement for notification

It's important to notify your employer as soon as possible to ensure your Right to Work records are updated. Employers are required to maintain accurate records, and this includes verifying that your new legal name matches the identification they have on file. This is essential for compliance with the Equality Act 2010. If you're a company director or a Person with Significant Control (PSC), you also have a legal duty to inform Companies House within 14 days by submitting form CH01.

If you're part of a regulated profession, like those overseen by the GMC, SRA, or NMC, you must also inform your professional body to ensure your licences and registrations align with your new legal name.

Impact on financial or legal documentation

Your payslips, P60s, and P45s must display your updated legal name to match HMRC records. While your National Insurance number will remain unchanged, failing to update your name could cause issues, such as contributions being misattributed. This could risk your state pension and benefit entitlements down the line. Similarly, workplace pension providers need your updated details to correctly link your retirement savings to your new identity.

If you have professional indemnity insurance, it's critical to update your policy immediately. Not doing so could be considered "non-disclosure", which might void your coverage when you need it most.

Ease of updating records

To update your records, provide your deed poll to your HR or Payroll department straight away. You'll need to present the original deed poll so they can make a copy for their files. Once this is done, they'll update internal systems, including your email address, ID badge, and company directory. Be sure to request written confirmation, such as an updated payslip, as proof of the change. After this, you can proceed with updating other organisations to ensure all your records are consistent with your new legal name.

6. Utility Companies (Gas, Electricity, Water)

Impact on financial or legal documentation

Keeping your utility accounts updated is just as important as notifying government and financial institutions when you change your name. Overlooking this step can lead to unnecessary complications.

If your utility providers aren't informed, it could trigger an 'Identity Ripple Effect' across your accounts. This might result in issues like failed Direct Debits, unpaid bills, late fees, or even disconnection of services. While there's no specific law requiring you to notify utility companies of a name change, deliberately avoiding this to escape debts or legal obligations is illegal. Keeping your records updated ensures transparency and avoids any misunderstandings about your financial responsibilities.

Ease of updating records

Updating your details with utility providers is generally a simple process. Most major suppliers - such as British Gas (0330 100 0056), EDF Energy (0333 200 5100), E.ON Energy (0345 052 0000), SSE (0345 070 7373), Octopus Energy (0808 164 1088), OVO Energy (0330 303 5063), and Scottish Power (0800 027 0072) - offer online or phone options. Log into your online account, go to the 'Personal Details' or 'My Account Details' section, and submit a name update form. You'll typically need your account number, postcode, and a copy of your deed poll. Most providers accept a photocopy or digital scan of the document.

For water suppliers, the process is slightly different since you can't switch providers. You'll need to contact your regional supplier directly, either online or via their customer service line. It's a good idea to update your primary identification documents - like your passport, driving licence, and bank account - first. Utility companies often ask for these as additional verification along with your deed poll.

To stay organised, keep track of the dates you notify each provider and note any reference numbers. This way, you can ensure that all updates are completed without any hiccups.

Next up, we'll look at how to change your name with other service providers to wrap up your name change process.

7. Council Tax Office

Impact on financial or legal documentation

Your council tax bill is more than just a payment reminder - it’s a recognised piece of evidence for your new name. The HM Passport Office accepts it as "proof of name use", which is essential for verifying your identity when applying for a passport. It demonstrates that you’re consistently using your new name across various aspects of your life.

The HM Land Registry also considers a current-year council tax bill as valid identity evidence (List B) when updating property titles. If you own property, ensuring your council tax bill reflects your updated name can save you from complications during title transfers or property registration.

Ease of updating records

Updating your Council Tax records is straightforward and can usually be done online, via email, or over the phone. Councils like Buckinghamshire and Central Bedfordshire provide these options. To start, you’ll need your Council Tax account reference number, which is typically 8 or 9 digits long and can be found on previous bills or correspondence.

Simply log into your council’s online portal, navigate to the personal details section, and upload your deed poll to legally change your name. Alternatively, you can email or call your council directly to make the changes. However, keep in mind that updating your details with HMRC or other government bodies doesn’t automatically update your Council Tax records - this must be done separately with your local council.

Potential consequences of failing to notify

While there’s no legal deadline or penalty for not updating your Council Tax records, failing to do so can lead to unnecessary complications. Without an updated council tax bill, you may struggle to provide the required "proof of name use" for passport applications or property registration with the HM Land Registry. Additionally, mismatches between your legal name and council tax records can cause issues when using the bill as secondary identification for financial or legal matters. To avoid these headaches, it’s best to update your records promptly.

8. Insurance Providers (Car, Home, Life)

Legal Requirement for Notification

While it’s not legally required to inform your insurance providers about a name change, neglecting to do so can lead to serious problems. For instance, car insurance policies must match the name on your driving licence. If your licence is outdated, you could face a fine of up to £1,000, and worse, your coverage could be voided, leaving you without protection.

Impact on Financial or Legal Documentation

When making a claim, insurers will check your identity against official documents. If your policy name doesn’t align with your passport, driving licence, or other legal records, your claim might be denied. This is especially critical for private health insurance, where accurate records are essential for processing claims and referrals.

Ease of Updating Records

Updating your name with most insurance providers is usually simple. You can contact customer service, fill out an online form, or send a written request. Be prepared to provide your policy or account number and a copy of your deed poll - some providers may ask for a certified copy. It’s a good idea to update documents like your passport, driving licence, and bank account first, as these are often used for verification.

Potential Consequences of Failing to Notify

If you don’t update your details, you could face several challenges. Claims may be denied, and outdated information could cause financial discrepancies. Credit agencies like Experian might flag these inconsistencies, potentially affecting your credit score. If you hold professional indemnity insurance tied to a professional register (e.g., GMC, SRA, or NMC), ensure those records are updated too. Keep a detailed record of all communications with insurers, noting dates and reference numbers, to stay organised.

Keeping your insurance details consistent with your other documents is crucial to avoid complications. Once done, it’s time to ensure your healthcare records are up to date as well.

9. Healthcare Providers (GP, Dentist, NHS Records)

Legal Requirement for Notification

Keeping your healthcare providers informed about a name change is crucial for ensuring your medical records remain accurate. According to the UK GDPR 2021, healthcare providers must maintain up-to-date personal data. If you've changed your name due to marriage or by deed poll, the Department of Health and Social Care requires you to provide your GP with proof of the change, such as the relevant document. For healthcare professionals, like doctors or pharmacists, there's an added layer of responsibility. You're legally and professionally obligated to notify regulatory bodies like the General Medical Council (GMC) or the General Pharmaceutical Council (GPhC) to ensure public registers are accurate.

Impact on Financial or Legal Documentation

Your GP surgery acts as the central point for managing your NHS records. Once your GP updates your information, it often triggers changes across your NHS profile. However, this doesn't cover everything - you'll need to inform your dentist and any specialised clinics you visit separately. Don’t forget to update your EHIC (or GHIC), as outdated details could complicate travel-related healthcare. Keeping all your records consistent is as important here as it is for other official documents.

Ease of Updating Records

Many GP practices now offer online portals where you can update personal details, including your name. This makes the process more convenient. While most healthcare organisations accept photocopies of your proof documents, some regulatory bodies, like the GMC, may require original documents. For example, the GMC might need to see both your old and new passports rather than just a deed poll.

Potential Consequences of Failing to Notify

Failing to update your records can lead to serious issues. Treatment could be delayed due to discrepancies in your records, and during emergencies, mismatched names might prevent hospitals from identifying you to your relatives. Administrative errors can also arise, including problems with billing, insurance claims, or healthcare transactions. Even minor mistakes, like a wrong name on a form, can result in privacy breaches or the improper sharing of sensitive information. These errors need to be corrected quickly, usually within 30 days, to avoid further complications.

10. Mortgage or Loan Providers

Legal Requirement for Notification

If you've changed your name, mortgage and loan providers will need a wet-ink signed, unenrolled deed poll signed by witnesses as formal proof under AML (Anti-Money Laundering) and KYC (Know Your Customer) regulations. Until you notify them, your financial liabilities and credit file will remain tied to your old name. Most lenders insist on receiving the original deed poll with a wet-ink signature, as photocopies or digital scans are rarely accepted.

Impact on Financial or Legal Documentation

Updating your mortgage account is crucial to avoid what’s known as an 'Identity Ripple Effect'. This can lead to disrupted direct debits and fragmented credit histories. Keeping your records consistent ensures credit agencies like Experian and Equifax can correctly link your old and new names, preserving your credit score. It's worth noting that the process for updating records varies depending on your lender.

Ease of Updating Records

Different lenders have different procedures. High-street banks like Lloyds, HSBC, or Barclays often require you to visit a branch in person with your original deed poll and photo ID. In-branch updates are usually handled on the spot. If you're sending documents by post, Royal Mail Special Delivery is recommended, and processing typically takes around two weeks. The good news? Most UK lenders update your name at no additional cost.

Potential Consequences of Failing to Notify

Failing to update your name can lead to more than just payment and credit score issues. For instance, if your mortgage is connected to a protection policy, such as life or home insurance, a name mismatch could result in a claim being denied. Homeowners should also be aware of the Land Registry. While your lender will update your mortgage account, this doesn’t automatically update your name on the Land Registry. Many people delay this step until they sell or remortgage their property, as it often requires a solicitor. However, keeping your mortgage and Land Registry records aligned can prevent future legal complications.

How to Notify Organisations of Your Name Change

The process of notifying organisations about your name change is relatively simple, though the exact steps can differ depending on the institution. Start with key documents like your Passport, Driving Licence, and Primary Bank Account if you change your last name. Once these are updated, they become reliable proof of identity, making it much easier to update smaller organisations. For example, utility providers often accept a new passport or driving licence as evidence, which might mean you won’t need to present your deed poll.

Get your documents in order. High-security organisations like HM Passport Office or banks usually require your original deed poll or a solicitor-certified copy. They won’t accept photocopies or digital scans. On the other hand, most other organisations, such as healthcare providers and utility companies, are fine with a simple photocopy. If you need to notify multiple organisations, consider using certified copies to avoid sending out your only original deed poll. Services like Name Change can provide certified copies along with tracked delivery to help with this.

Notification procedures differ. For example, HMRC allows you to update your details online via the Government Gateway. Banks often require you to visit a branch in person with your deed poll and photo ID, but some may accept certified copies sent through secure post. The DVLA requires you to fill out and post Form D1 along with your original deed poll. For the Passport Office, you’ll need to apply online and then send your original document via secure post. After completing these updates, make sure to keep a record of each notification.

Keep track of everything. Maintain a log with the date, method, and any reference numbers for every update. This could save you time if there are any follow-up issues. Also, updating your name with banks and the electoral roll automatically informs credit reference agencies like Experian and Equifax, so you don’t need to contact them separately.

Hold onto your deed poll as a permanent record of your name change. This is especially important for linking older documents, like exam certificates or degrees, to your new name. Educational institutions typically won’t reissue qualifications with a new name unless the change is related to gender transition. Your deed poll will serve as proof that these records are still yours.

Conclusion

Letting organisations know about your name change is a crucial step to sidestep potential issues. For instance, having an outdated driving licence could lead to fines of up to £1,000, while mismatches with insurance records might even invalidate claims. On top of that, inconsistent records can fragment your credit file and disrupt direct debits.

If you don’t inform HMRC or your employer, you risk incorrect tax codes, which could affect your State Pension. And travelling with a passport that doesn’t match your new name might leave you stranded at the airport. It's also worth noting that failing to update records deliberately to dodge debts is considered fraud.

To make the process smoother, tackle it systematically. Start with the "Power Trio" - your Passport, Driving Licence, and Primary Bank Account - as these are often the key documents needed to update other records.

FAQs

What order should I update organisations in after a deed poll?

After receiving your deed poll, the first step is to update your details with key government agencies such as HMRC, the DVLA, and the Passport Office. This ensures your official identification and legal documents reflect your new name.

Next, inform your financial institutions, including banks and building societies, as well as utility companies and communication service providers.

Finally, make sure to notify healthcare providers, local councils, schools or universities, and any private organisations where you hold memberships, subscriptions, or insurance policies. Prioritising updates in this way helps ensure that the most critical changes are made first.

Do I need to send my original deed poll or will a certified copy do?

When dealing with a name change, most organisations will ask for your original deed poll as proof. That said, some may accept a photocopy instead. For example, government bodies like HM Passport Office usually insist on seeing the original document. It's always a good idea to double-check with the organisation in question to understand their specific requirements.

How do I stop my credit file being split after a name change?

To keep your credit file intact after changing your name, make sure you inform all relevant financial institutions - like your banks, credit card companies, and lenders - so they can pass the updated information to credit reference agencies. Don’t forget to update your details on the Electoral Roll through your Local Authority as well.

It’s also a good idea to regularly review your credit file to check for any errors. If you spot inaccuracies, you can request corrections under GDPR to ensure your credit history stays consistent and accurate.