Pension vs Insurance: Name Change Processes

If I change my name in the UK, I’d update my pension and insurance records at the same time. That cuts the risk of payment issues, claim delays, and mismatched records.

Here’s the short version:

- Both pensions and insurers usually ask for the same proof:

- unenrolled deed poll

- marriage or civil partnership certificate

- decree absolute or final order

- Pension updates are often more formal:

- workplace schemes may go through HR or payroll

- private pensions often need the provider’s admin team

- State Pension is handled by the DWP

- Insurance updates are often simpler:

- many motor, home, and travel insurers allow changes online or by phone

- life and health cover often need more checks

- Delays matter:

- with pensions, they can affect records, tax handling, or payments

- with insurance, they can slow renewals or claims

A name change is common, but admin can still drag. In 2024, there were over 270,000 marriages in England and Wales in recent annual figures, which means many people still need to update old records after a change of name.

Quick Comparison

| Point | Pension providers | Insurance companies |

|---|---|---|

| Main contact route | Employer, provider admin team, or DWP | Online account, phone, or post |

| Proof usually accepted | Deed poll, marriage certificate, civil partnership certificate, divorce record | Deed poll, marriage certificate, civil partnership certificate, divorce record |

| Checks | Often stricter | Often lighter for general cover |

| Time to update | Often slower | Often faster for general policies |

| Risk if left wrong | Payment and tax issues | Claim and renewal issues |

My takeaway: the required documents are much the same, but the route and wait time often differ. If I keep my policy numbers, member numbers, scans, and certified copies ready, the job is usually far less awkward.

sbb-itb-bf1bef6

How to change your name with a pension provider

Changing your name on a pension usually comes down to two things: the type of scheme you have and how that provider runs its admin. Some providers still want documents sent by post. Others now accept secure online uploads.

Workplace, private and State Pension: different routes

The process depends on the kind of pension you hold.

For a workplace pension, start with your employer’s HR or payroll team. If your employer entered the wrong name in the first place, they may be able to fix it through payroll. Not sure who deals with it? Check your scheme’s welcome pack for the right admin team.

With private pensions, including SIPPs and personal pensions, you’ll usually deal with the provider directly. Contact the admin team linked to your policy. This bit matters: large providers sometimes handle older policies through a separate admin team, so it’s worth checking the right contact before you ring.

The State Pension is dealt with separately through the DWP.

What evidence pension providers ask for

Once your request reaches the right admin team, the proof they ask for is usually fairly simple. Most providers want original documents or certified copies, although some now accept secure digital uploads.

If you’re still paying into a workplace scheme, a payroll update may be enough. If you’re already taking the pension, write to the provider and include the legal document.

Be clear about the exact name you want on record: your married name, your current name, or a hyphenated version.

How to change your name with an insurance company

Insurance updates are often more direct than pension updates, although the process still depends on the type of policy you have. In the UK, insurers will often let you request a name change through an online portal, by phone or by post. For straightforward policies, general insurance updates are usually dealt with fairly fast.

General insurance versus life and health policies

For motor, home and travel insurance, many providers let you change your name through your online account or over the phone. In some cases, you won't need to send any documents, provided you have already legally changed your name. That said, some insurers will still ask for proof, depending on their own rules.

Life, critical illness and private health insurers tend to be stricter. They usually ask for formal evidence of your name change before they update your record. You can often begin the process online or by phone, but the insurer may still need to check the change before it goes through. Updating your name is usually free.

Checking all your active policies

Make sure you update every active policy, not just one. If your policy name, payment details and ID don't match, that can delay a renewal or a claim.

This catches people out more often than you'd think. A large insurer may handle different products through separate teams, and older policies can still sit under a legacy brand. That's why it's worth checking your policy schedule so you contact the right team, especially for older cover.

Once the change has been made, ask for written confirmation that your records, including renewal documents, now show your legal name.

That difference is what the comparison with pensions comes down to.

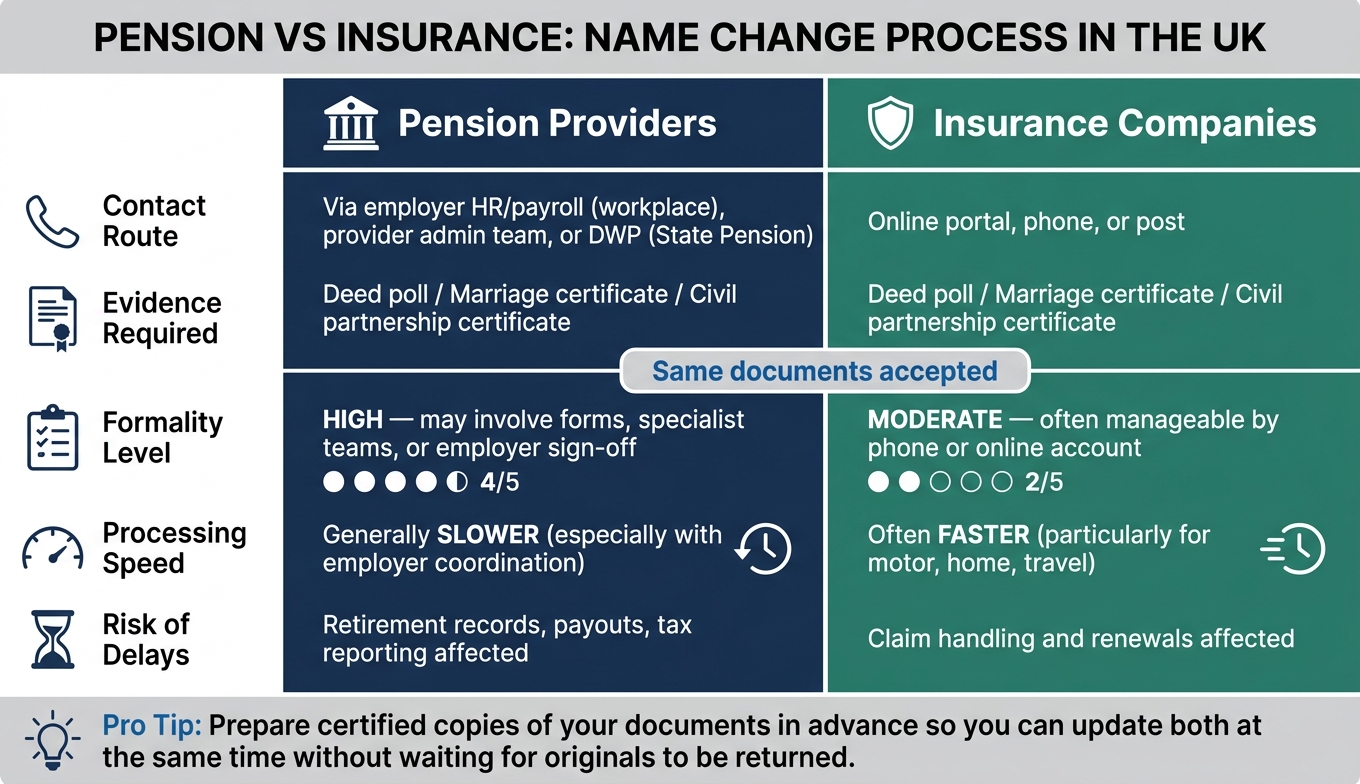

Pension vs insurance: how the processes compare

Pension vs Insurance Name Change: UK Process Comparison

Once you get past the step-by-step admin, the main gap comes down to how each provider checks your documents and handles the change. Both pensions and insurance firms need legal proof of your new name, but the process - and the time it takes - can feel quite different.

Where the two processes are the same

If you're updating a pension or an insurance policy, the documents are much the same. Both will usually accept a deed poll, marriage certificate or civil partnership certificate. In both cases, it also helps to have your account, member or policy number ready before you make contact. That small bit of prep can save a lot of back-and-forth.

Where the two processes differ

The biggest differences are formality and speed. Insurance, especially general cover like motor or home insurance, is often the simpler job. In many cases, you can sort it by phone, post or through an online account.

Pension providers tend to be more formal. They may ask you to fill in forms, deal with a specialist team, or go through your employer if it's a workplace scheme. That can slow things down, especially when more than one party needs to sign off the update.

| Feature | Pension Providers | Insurance Companies |

|---|---|---|

| Contact Route | Often via employer for workplace schemes, or through forms and provider contact | Online portal, phone or post |

| Evidence Required | Deed poll, marriage certificate or civil partnership certificate | Deed poll, marriage certificate or civil partnership certificate |

| Formality | High - may involve forms or follow-up from a specialist team | Moderate - often manageable by phone or online account |

| Processing Speed | Generally slower, especially where employer coordination is needed | Often faster, particularly for general insurance |

| Impact of Delays | Can affect retirement records, payouts and tax reporting | Can affect claim handling if policy details do not match |

That side-by-side view makes one thing clear: being organised helps in both cases.

Getting your documents ready and wrapping up

Once you know which provider is likely to ask for more paperwork, get everything ready before you contact either one.

A simple document checklist

It’s easier to sort your paperwork in one go. First, find the right proof of your name change: a deed poll, marriage certificate, civil partnership certificate, or decree absolute. Keep a clear scan or PDF for your own records before you post anything.

Then check how each provider wants to receive it. Some ask for a secure upload. Others may want a certified copy or the original document.

If you need to tell several organisations at the same time - say, a pension provider and an insurer - it can help to order more than one certified copy. That way, you’re not stuck waiting for one original to come back before sending it elsewhere. Name Change offers unenrolled deed polls with certified copies, which can make it simpler to keep your documents in order for different UK organisations.

Use tracked post so you have proof of delivery.

Once your paperwork is ready, the main difference is simply how each provider deals with the update.

Key points to take away

Both providers need legal proof of your new name. Pension providers tend to be more formal. General insurance providers are often quicker.

FAQs

Should I update my pension or insurance first?

It’s usually best to update your insurance first and your pension records after that.

Keeping your insurance details up to date can help you avoid problems with cover or claims. Once that’s done, contact your pension providers so your contributions and future benefits are recorded under your new name.

That way, your records stay aligned, and you’re less likely to run into admin issues later.

What if my insurer changes my name but my pension provider doesn’t?

If your insurer updates your name but your pension provider does not, you’ll need to contact each one separately. That’s the only way to keep your records accurate and consistent.

Get in touch with your pension provider directly, because HMRC will not update pension records for you. Keeping your pension details up to date helps make sure your entitlement and benefits are correct.

Do I need certified copies for every provider?

No. Most organisations will accept a photocopy of your deed poll, or other proof of your name change, for routine updates.

That said, some providers may ask for the original deed poll or certified copies, especially for more formal or sensitive checks. It comes down to that organisation’s own requirements.